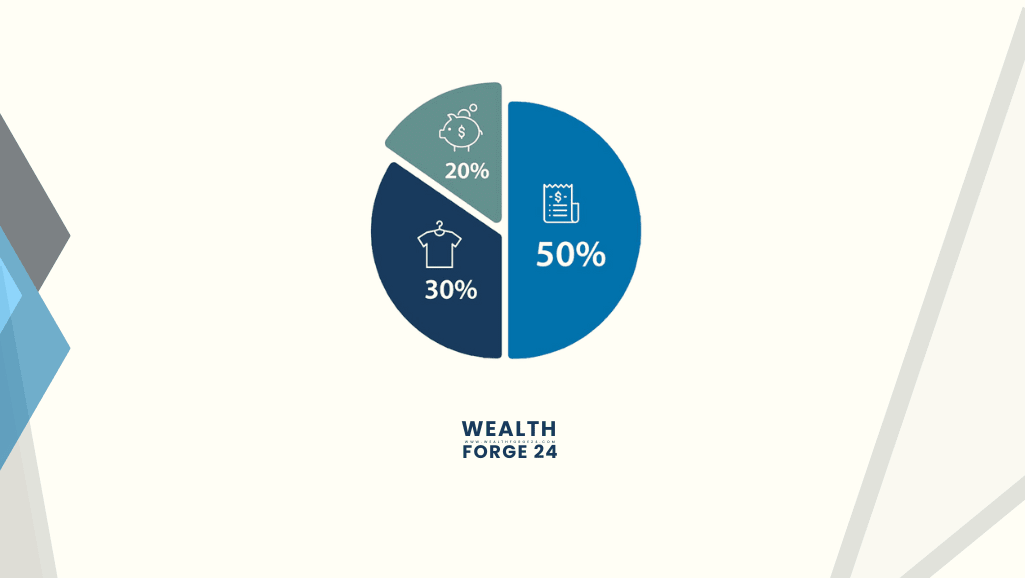

Smart private finance is about balancing needs and saving for the future. The 50/30/20 rule is a memorable rule of thumb that allows you to do all three.

Experts define the 50/30/20 rule.

The 50/30/20 budget was created by Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi. In their book, *All Your Worth: The Ultimate Lifetime Money Plan* 💰, they explain it. Warren wrote it while teaching at Harvard Law.

The 50/30/20 price range is primarily based on after-tax profits and stipulates that spending:

- 50% of your profits are for needs.

- 30% of your earnings go to wishes.

- 20% of your earnings go to savings.

The technique won recognition for its simplicity. Just remember three simple numbers. No spreadsheets, pivot tables, or tricky rules to learn! As long as you keep those three numbers in mind during the month, you’ll budget quite efficiently.

50% for desires

Needs are mandatory prices that you, without a doubt, can’t pass up. Things like groceries, rent, childcare—you understand, “adulting” stuff.

Here’s a general listing of spending categories that fall into the needs bucket:

- Rent/loan

- Utilities

- Insurance rates (vehicle, home, medical, and many others)

- Groceries

- Transportation (gas, bus fare, etc.)

- Wi-Fi and mobile record plans

- Therapy and intellectual fitness services

- Gym membership, which some may consider essential, exists alongside free ways to work out.

30% for wants

The center spending category is “wants.” These are things that can improve your lifestyle, but you don’t have to buy them every month.

Things that fall into the desires category encompass, but aren’t restricted to:

- Restaurants and takeout

- Entertainment and media subscriptions (Twitch, Netflix, etc.).

- Travel

- Concert and film tickets

- Online buying

- Fashion

- Video games and consoles

- Alcohol

Have you grasped the point? And yeah, every so often, it is hard to distinguish between a “want” and a “want.” We’ll talk more about that in a bit.

For now, let’s talk approximately about the closing class of the 50/30/20 budget: savings.

20% for savings

Everybody asks me many times how much of their profits they must save each month. The solution is right here: at least 20 percent. Most people will think of saving as diverting cash into a savings account. But you can count any of the following as savings:

- Contributions to a 401(k) or IRA.

- People deposit money into savings accounts or certificates of deposit.

- Other investments

- Payments made toward debt that exceeds the minimum monthly requirements.

50/30/20 finance example

Let’s say you are taking home $4,000 a month after taxes. Here’s a breakdown of what 50/30/20 finances might look like.

$4,000 x 50% = $2,000 for wishes

- $1,400 for hire and utilities

- $250 for groceries

- $150 for intellectual/physical fitness expenses

- $100 for mobile information and Wi-Fi.

- $one hundred for gas

$4,000 x 30% = $1,200 for wants.

- $400 for eating places and takeout

- $350 for shopping

- $250 for amusement

- $200 for vacation financial savings.

$4,000 x 20% = $800 for financial savings

- $400 into your 401(k)

- $250 in different long-term investments

- $100 goes into your emergency fund.

- $50 into speculative investments (crypto, man or woman shares, and many others).

What if you can’t keep 20%?

If you save far less than 20% of your profits, you’re like many others. Despite all the benefits of dwelling in the United States, our financial system makes it tougher and harder for most Americans to get ahead. Housing, meals, schooling, and healthcare fees cost an excessive amount, and jobs pay too little. Add a tradition that worships consumerism. It makes everyone feel they need the latest iPhone. This is a recipe for monetary disaster.

The 50/30/20 budget is becoming outdated. It was conceived in 2006, while the median hire in the United States was around $950. Today, it’s $2,000, and our cost of living keeps outpacing the salary boom.

You can trade the numbers! I heard someone suggest that the guideline needs to be updated to 60/30/10 as housing and other wishes get extra high-priced. That makes sense to me. You can play with ratios to arrive at a budget that works for you, so long as you’re making saving a priority. On the other hand, in case you’re very frugal, you may live on a 50/20/30 price range.

Pros and cons of the 50/30/20 pricing range.

Pros

- It’s easy. Some budgeting methods call for complex spreadsheets, pivot tables, and more. But a 50/30/20 finance plan can be worked out quickly.

- Budgeting apps align well with this approach. Many modern budgeting apps include the 50/30/20 plan. With just a tap, you can stay accountable. You’ll get notifications, tracking, and more.

- Saving 20% is competitive but extremely powerful. Here’s a TL;DR of that: Just save 20% of your profits for 30 years and you’re golden. The 50/30/20 budget aligns with that approach flawlessly.

Cons

- 50% won’t cover your desires.

- It may be tough to distinguish between needs and wants. Is hiring a non-public trainer a “want,” as it’s pointless? Or is it a “want” because it contributes to your physical and mental health? 50/30/20 budgeters should face these questions regularly.

- It’s now not designed for debt structuring. The 50/30/20 budget wasn’t made for debt repayment. This forces people to awkwardly fit their debt into the 20% savings category.

- It’s not the best for Dad and Mom. Childcare fees can be very high and often change unexpectedly, as any parent knows. Raising children may lower your personal fulfillment by 60% or even 70%.