Picture this: It’s 2015, and I’m sitting in my tiny studio apartment, staring at my laptop screen, about to click “buy” on my first $200 worth of Bitcoin. My hand was literally shaking. Not because I was afraid of losing the money—okay, maybe a little—but because I was stepping into something completely unknown.

Fast forward to today, and here I am, watching Bitcoin dance around $102,000. Yes, you read that right. One hundred and two thousand dollars. And you know what? People are still asking me the same question I asked myself back then: “Is it too late to start?”

The short answer? Absolutely not. But let me tell you the longer, more interesting story.

What’s Actually Happening Right Now (And Why It Matters to You)

November 2025 has been… intense. Bitcoin recently dipped below $100,000 for the first time since June, and the crypto Twitter-sphere went into full panic mode. But here’s what ten years in this space has taught me: These moments? They’re actually opportunities dressed up as scary headlines.

Let me back up a bit. After Donald Trump won the 2024 election, Bitcoin went on an absolute tear—soaring 60% and smashing through $111,000. We hit an all-time high of $126,210 on October 6, 2025. It was euphoric. Everyone and their grandmother was suddenly a crypto expert.

But markets don’t climb forever. They breathe. They pause. They test your patience. And that’s exactly what’s happening now. The total crypto market pulled back to $3.46 trillion, Ethereum dropped about 9% to $3,275, and suddenly everyone’s asking if the party’s over.

Spoiler alert: It’s not. This is just how markets work.

Let Me Explain Bitcoin Like You’re Sitting Across From Me at Coffee

You know what I love about Bitcoin? It’s simultaneously the simplest and most complex thing I’ve ever tried to explain.

Here’s the simple part: Bitcoin is digital money that lives on the internet. No bank controls it, no government can print more of it, and no one can take it away from you if you store it properly.

Now here’s where it gets interesting.

The Story of Satoshi and the Pizza That Changed Everything

In 2009, someone—or a group of someones—using the name Satoshi Nakamoto created Bitcoin. We still don’t know who they are, and honestly? That mystery adds to the magic. The first Bitcoin price ever recorded was around $0.00076. Less than a penny. Less than a fraction of a penny.

Then came May 22, 2010. A programmer named Laszlo Hanyecz was hungry. He offered 10,000 Bitcoins for two pizzas. Someone took him up on it. Those pizzas are now worth over $1 billion. Yes, billion with a B.

Every year, we celebrate “Bitcoin Pizza Day” and laugh nervously about it, while secretly calculating what our early purchases would be worth today.

How This Whole Thing Actually Works (Without Making Your Brain Hurt)

Think of Bitcoin as a massive public notebook that everyone can read but no one can erase or change. Every transaction ever made is written in this notebook, which we call a “blockchain.”

When you send Bitcoin to someone, thousands of computers around the world verify that you actually own those coins and that you’re not trying to spend them twice. Once verified, the transaction gets written into the notebook permanently.

The people running these computers? We call them “miners.” They solve incredibly complex math problems to verify transactions, and in return, they get rewarded with new Bitcoin. But here’s the catch—and this is crucial—the reward gets cut in half roughly every four years.

The most recent “halving” happened in April 2024, dropping the reward from 6.25 BTC per block to 3.125 BTC. This built-in scarcity is why Bitcoin tends to become more valuable over time. There will only ever be 21 million Bitcoin, and we’ve already mined about 20 million of them.

Here’s Something That Changed Everything for Me

When I started, I thought I needed to buy a whole Bitcoin. That felt impossible at $200, let alone today’s prices. But then I learned: Bitcoin is divisible down to eight decimal places. The smallest unit is called a “satoshi” (named after the creator), and it’s worth 0.00000001 BTC.

This means you can literally start with $10, $25, $50—whatever works for your budget. The entry barrier is entirely psychological.

So… How Much Should You Actually Invest?

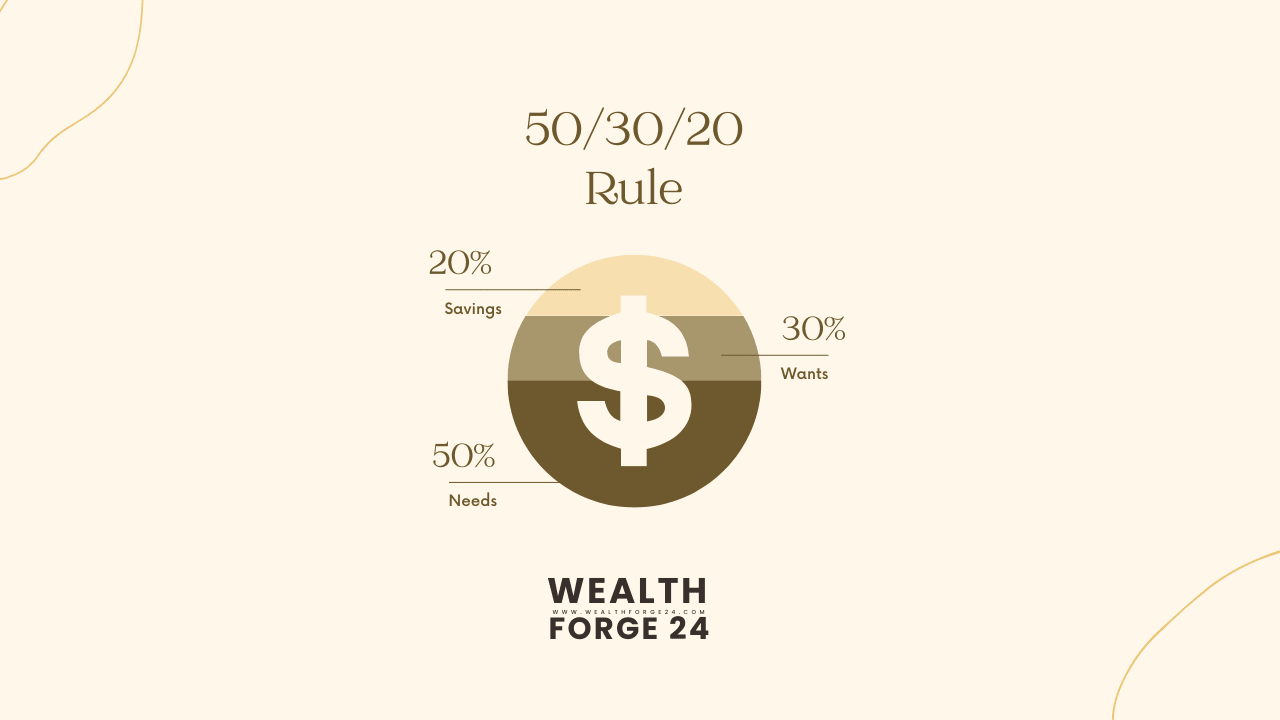

This is where I get real with you. After watching hundreds of friends, family members, and readers navigate this space, I’ve developed what I call the “Sleep Soundly Strategy.”

Rule #1: The Amount That Doesn’t Keep You Up at Night

Only invest money that you could lose tomorrow without it affecting your rent, groceries, or peace of mind. I’m serious about this.

In 2017, I watched Bitcoin rocket from $1,000 to nearly $20,000. I saw friends quit their jobs to day-trade crypto. Then came 2018, and Bitcoin crashed to $3,000. Those friends? Some lost their homes. The ones who invested their “extra” money? They held strong and are sitting pretty today.

The difference wasn’t their strategy—it was their stress level. The people who invested responsibly could afford to wait out the storm.

Rule #2: Start Small, But Start Now

Here’s my honest recommendation based on different comfort levels:

The Toe-Dipper ($50-$100): You’re curious but cautious. Perfect. This amount lets you learn how exchanges work, how wallets function, and how it feels to watch your investment bounce around without having a panic attack.

The Committed Beginner ($200-$500): You’ve done your homework and believe in Bitcoin’s long-term potential. This is enough to feel invested (literally) while building your knowledge and comfort level.

The Serious Starter ($1,000-$2,000): You understand the technology, believe in the vision, and have done extensive research. Just make sure this represents less than 5% of your total investment portfolio.

Rule #3: Dollar-Cost Averaging Is Your Secret Weapon

Here’s what I do, and what I recommend to everyone: Instead of trying to time the market (which is impossible), invest the same amount regularly.

For example, every Friday when I get paid, $100 automatically goes into Bitcoin. When the price is high, I get less Bitcoin. When it’s low, I get more. Over time, this averages out beautifully and removes all the emotional decision-making.

I started this strategy in 2018 when Bitcoin was at $6,000. I continued when it dropped to $3,000. I kept going when it climbed to $64,000. Today? That strategy has outperformed every “perfect timing” attempt I’ve ever made.

Before You Buy: Three Critical Questions to Ask Yourself

What Am I Actually Trying to Accomplish Here?

Be honest. Are you trying to:

- Get rich quick? (Dangerous mindset)

- Build long-term wealth? (Smart approach)

- Learn about new technology? (Excellent reason)

- Keep up with friends? (Terrible reason)

Your answer shapes your entire strategy. I’m a long-term holder. I believe Bitcoin will be worth significantly more in 5-10 years. This belief lets me ignore daily price swings and sleep peacefully.

Can I Handle the Rollercoaster?

Bitcoin once dropped 83% over two years. Let me repeat that: EIGHTY-THREE PERCENT. If you put in $1,000 at the peak, it became $170 at the bottom. Then it climbed back and eventually 10x’d that initial investment.

The people who made money? The ones who didn’t panic sell. The ones who lost? They sold at the bottom out of fear.

There’s a saying in crypto: “Time in the market beats timing the market.” It’s not just a catchy phrase—it’s backed by a decade of data.

What’s Happening in the Bigger Picture?

Right now, we’re in interesting times. The Federal Reserve is being cautious with interest rates, which typically means less money flowing into risky assets like crypto. The U.S. dollar is strong, Treasury yields are up, and some analysts are nervous.

But—and this is a big but—Bitcoin ETFs launched in 2024, bringing billions in institutional money. The Trump administration has taken a pro-crypto stance. Major banks are now offering Bitcoin services. The infrastructure around crypto is stronger than it’s ever been.

Yes, there are over 36 million different tokens out there now, and most are garbage. But Bitcoin remains the foundation, the standard, the one everyone points to.

Your Step-by-Step Guide to Actually Buying Bitcoin (Like I’m Right There With You)

Okay, you’ve decided to take the plunge. Let me walk you through this exactly how I’d guide my own sister.

Step 1: Picking Your Exchange (Where You’ll Buy Bitcoin)

Think of an exchange like a crypto marketplace. You’re trading your dollars for Bitcoin. After trying probably two dozen platforms over the years, here are my top recommendations:

For Complete Beginners: Coinbase

- Super user-friendly interface

- Excellent customer support (actually responds!)

- Regulated and trustworthy

- The trade-off? Higher fees (around 1.5%)

- My take: Worth paying extra for peace of mind when you’re learning

For Cost-Conscious Learners: Kraken

- Lower fees (0.16% to 0.26%)

- Strong security track record

- Great educational resources

- Slightly steeper learning curve

- My take: Once you’re comfortable, this is where I’d move

What I Look for in Any Exchange:

- Regulated in the U.S. (seriously, don’t mess with sketchy offshore platforms)

- No major hacking history

- Responsive customer service

- Clear fee structure

- Easy-to-use mobile app

Step 2: Setting Up Fort Knox-Level Security

This is where most beginners cut corners, and it breaks my heart when I hear about hacked accounts. Let me make this painfully clear: your security setup is more important than your investment strategy.

Two-Factor Authentication (2FA) – Non-Negotiable: Download Google Authenticator or Authy. Never, ever use SMS-based 2FA. Why? Because hackers can clone your phone number. It’s happened to friends of mine. Use an authenticator app.

Password Management: I use 1Password (there are others like LastPass or Bitwarden). Create a unique, randomly generated 20+ character password. Write it down on paper and store it somewhere safe. I’m serious about the paper backup—don’t rely solely on digital storage.

Email Security: Your exchange account is only as secure as the email attached to it. Make sure your email has 2FA enabled too. I’ve seen people secure their exchange perfectly, then get hacked through their email account.

Step 3: Making Your First Purchase (The Exciting Part!)

Alright, here we go:

Deposit Money:

- Bank transfer (ACH): 3-5 days, lowest fees, my preferred method

- Debit card: Instant, higher fees (around 3.99%), good for urgent purchases

- Wire transfer: Same day, moderate fees, good for large amounts

Buy Your Bitcoin:

- Navigate to “Buy/Sell” or “Trade”

- Select Bitcoin (BTC)

- Enter your amount (in dollars, not Bitcoin—it’ll calculate the BTC for you)

- Review the total including fees

- Take a deep breath

- Click confirm

- Screenshot the confirmation for your records

What Happens Next: The Bitcoin appears in your exchange wallet within minutes. Congratulations! You now own a piece of digital history. But we’re not done yet…

Step 4: Moving to Your Personal Wallet (This Is Critical)

Here’s where I see beginners make their biggest mistake. They buy Bitcoin and just leave it on the exchange. Then they wonder why I’m frantically waving my arms saying “NOOOOO!”

Remember: “Not your keys, not your coins.” If the exchange gets hacked, goes bankrupt, or freezes your account (all of which have happened to major platforms), your Bitcoin could disappear.

Understanding Wallets: Where Your Bitcoin Actually Lives

Let me break this down simply.

Exchange Wallets (Where Your Bitcoin Starts)

Think of this like keeping money in someone else’s safe. It’s convenient for trading, but you don’t actually control it. The exchange holds the keys. If they go down, your Bitcoin goes with them.

I keep maximum $500 on exchanges—only what I’m actively trading or planning to buy more with soon.

Software Wallets (Hot Wallets)

These are apps on your phone or computer—like Exodus, Trust Wallet, or Electrum. They’re connected to the internet, which makes them convenient but vulnerable.

I use these for my “spending money”—amounts under $1,000 that I might need to access quickly.

Hardware Wallets (Cold Storage – Your Best Friend)

These are physical devices that look like USB drives. Your private keys never touch the internet. Even if your computer is completely compromised with viruses, your Bitcoin stays safe.

Popular options:

- Ledger Nano X ($149): User-friendly, supports tons of cryptocurrencies

- Trezor Model T ($219): Open-source, excellent reputation

- Material Bitcoin (pricing varies): Non-electronic option, maximum security

My Personal Setup:

- Daily spending money ($200-500): Software wallet

- Medium holdings ($500-5,000): Hardware wallet at home

- Long-term holdings (everything else): Hardware wallet in safe

Setting Up Your Hardware Wallet (Step-by-Step)

- Buy directly from the manufacturer – Never buy used or from third-party sellers

- Verify the device is sealed – Check for tampering

- Initialize it yourself – Never use a device that comes with a pre-configured seed phrase

- Write down your recovery phrase – 12 or 24 words that can restore your Bitcoin

- Triple-check your writing – One wrong letter means lost Bitcoin forever

- Store the phrase securely – I keep copies in two different physical locations

- Never take a photo of it – Never store it digitally anywhere

The Mistakes That Still Haunt Me (So You Don’t Have to Make Them)

The Scams I’ve Seen Break Hearts

The “Double Your Bitcoin” Scam: In 2020, my friend saw a Tweet from what looked like Elon Musk’s account: “Send 1 BTC, get 2 BTC back!” The account was hacked. She sent $8,000 worth of Bitcoin. Gone forever. The rule: No legitimate person will ever ask you to send crypto to get more back.

The Fake Exchange Website: Another friend tried to log into Coinbase. The URL was coinbase-login.com instead of coinbase.com. He entered his credentials. Within 20 minutes, his account was drained. Always bookmark your exchange site and only use that bookmark to log in.

The “Urgent Security Alert” Email: “Your Binance account has been compromised! Click here to secure it immediately!” The email looked perfect—logo, formatting, everything. It was fake. The link installed malware. Now I have a rule: Never click links in crypto-related emails. Always go directly to the website yourself.

The Telegram “Support” Team: You post a question in a crypto group. Immediately, three people DM you claiming to be customer support. They want to “help” by accessing your wallet. Real exchanges never DM you first. Ever.

The Emotional Mistakes That Cost Me Real Money

FOMO Buying at the Top (2017): Bitcoin hit $19,000. Everyone was talking about it at Christmas dinner. I bought $2,000 more at $18,500 because I was terrified of missing out. It crashed to $3,000 over the next year. I learned: Buy when no one’s talking about it, not when everyone is.

Panic Selling at the Bottom (2018): When Bitcoin dropped to $6,000, I sold some, convinced it was going to zero. It eventually went to $69,000. I learned: Never make decisions based on fear. Have a plan and stick to it.

Overtrading (2019): I tried day trading for three months. Made 30+ trades. At the end, I was down 15% after fees, while Bitcoin was up 12%. I learned: Trading fees and taxes eat away profits. Buy and hold beats active trading for most people.

Keeping Everything on an Exchange (2020): I kept $10,000 worth of Bitcoin on a smaller exchange. They got hacked. I lost $3,500 before they partially reimbursed customers. I learned: Move your Bitcoin to personal storage immediately.

The Tax Reality Nobody Likes Talking About

Here’s something most crypto content skips: the IRS treats Bitcoin as property, not currency. This has major implications.

Every Time You Sell, Trade, or Spend Bitcoin, It’s Taxable:

- Sell Bitcoin for USD? Taxable.

- Trade Bitcoin for Ethereum? Taxable.

- Buy a pizza with Bitcoin? Taxable.

What You Need to Track:

- Date and price of every purchase

- Date and price of every sale

- Every trade between different cryptocurrencies

- All fees paid

- The “cost basis” of each transaction

My System: I use CoinTracker ($99/year). It connects to my exchanges and wallets, automatically tracks everything, and generates tax reports. I tried doing it manually my first year. Never again. The spreadsheet nightmares still haunt me.

Capital Gains Tax Rates:

- Hold less than one year: Taxed as ordinary income (up to 37%)

- Hold more than one year: Long-term capital gains (0%, 15%, or 20% depending on your income)

This is another reason why long-term holding makes sense—better tax treatment.

What I’m Watching Right Now (November 2025 Edition)

The market is at an interesting inflection point. Let me share what’s on my radar:

The Bullish Signs

Institutional Adoption Is Real: The Bitcoin ETFs aren’t just financial products—they’re a psychological shift. Traditional investors can now buy Bitcoin through their regular brokerage accounts. As of today, these ETFs hold billions in Bitcoin.

The Trump Effect: Love him or hate him, Trump’s pro-crypto stance has brought regulatory clarity. The SEC is backing off aggressive enforcement. Major banks are launching crypto services without fear of regulatory crackdown.

The Halving Aftermath: History shows Bitcoin typically rallies 12-18 months after each halving event. April 2024’s halving puts us right in that window. The pattern has held for three previous cycles.

Stablecoin Growth: Stablecoins processed over $8 trillion in transactions last year. That’s not speculation—that’s real utility, real adoption, real proof that crypto infrastructure works.

The Bearish Concerns

The “Higher for Longer” Fed: If interest rates stay elevated, money tends to flow out of risky assets and into safe Treasury bonds. Bitcoin, despite maturation, is still considered a risk asset.

Market Oversaturation: There are literally 36 million different tokens now. Most are worthless. This dilutes attention and capital away from quality projects like Bitcoin. The days of “everything goes up” are over.

Geopolitical Uncertainty: Global tensions affect all markets. When investors get scared, they often sell everything risky first, ask questions later.

Technical Indicators: Bitcoin’s monthly MACD (a momentum indicator) is showing consolidation. We might trade sideways for a while before the next major move up or down.

My Honest Assessment

I think we’re in a healthy consolidation phase. Bitcoin briefly dropping below $100,000 after months above it isn’t alarming—it’s normal profit-taking. The fundamentals remain strong. The adoption continues. The infrastructure improves daily.

Could we drop to $80,000? Sure. Could we rally to $150,000? Absolutely. Can anyone tell you with certainty? Nope.

That’s why dollar-cost averaging works. It removes the need to predict the unpredictable.

My Personal Strategy (Full Transparency)

I’m often asked what I’m actually doing with my own money. Fair question. Here’s my exact approach:

Portfolio Allocation:

- 65% Bitcoin (long-term hold, hardware wallet)

- 25% Ethereum (I believe in smart contracts)

- 8% stablecoins (dry powder for dips)

- 2% experimental altcoins (learning, not investing)

Investment Rhythm:

- $100 every Friday into Bitcoin (automatic, no emotion)

- $50 every Friday into Ethereum

- Extra lump sums during 15%+ dips (if I have spare cash)

Rules I Never Break:

- Never invest money needed within 3 years

- Never use leverage or margin trading

- Never check prices more than once daily

- Never make investment decisions after 9 PM (tired brain makes bad choices)

- Never discuss specific dollar amounts publicly (security risk)

My 5-Year Plan: I’m accumulating until 2027, then reassessing. My belief is that Bitcoin will be significantly higher by 2030. If I’m wrong? The amount I’m investing won’t change my life. If I’m right? It could change everything.

Your Bitcoin Journey: Next Steps

You’ve made it this far, which means you’re serious about this. Here’s exactly what I want you to do next:

This Week:

- Open an account on Coinbase or Kraken

- Complete identity verification

- Set up 2FA using an authenticator app

- Make your first small purchase ($50-$100)

This Month:

- Research hardware wallets

- Order one (directly from manufacturer)

- Transfer your Bitcoin off the exchange

- Set up your recovery phrase backup system

- Start your dollar-cost averaging schedule

This Year:

- Continue regular investments

- Learn about Bitcoin’s technology (try reading “The Bitcoin Standard”)

- Join quality crypto communities (avoid pump-and-dump groups)

- Track your investments for tax purposes

- Reassess your strategy quarterly

The Real Answer to “How Much Should I Buy?”

After all this, here’s my final answer: Buy an amount that lets you sleep soundly, learn actively, and hold patiently.

For most beginners, that’s $100-$500 to start, followed by $50-$200 monthly recurring purchases.

The magic isn’t in the amount—it’s in the consistency and the long-term thinking.

Bitcoin isn’t a get-rich-quick scheme. It’s a get-rich-slowly opportunity for those patient enough to understand it, brave enough to hold through volatility, and smart enough to secure it properly.

FAQ (The Real Ones)

“Is $100 really enough to make a difference?”

At current prices, $100 gets you about 0.001 BTC. If Bitcoin reaches $1 million (which some analysts predict by 2030), that’s $1,000. Not life-changing, but a 10x return. More importantly, it gets you started learning.

“What if I buy and it immediately crashes?”

It probably will at some point. Bitcoin’s dropped 50% or more multiple times. That’s why you only invest what you can afford to lose and commit to holding long-term. Crashes are temporary; the upward trend has been consistent over any 4-year period.

“Should I tell people I own Bitcoin?”

No. Seriously, no. It makes you a target for scams, hacking attempts, and that annoying cousin who wants investment advice at Thanksgiving. Keep it private.

“Can I still buy Bitcoin if I’m not tech-savvy?”

Absolutely. Modern exchanges are as easy to use as any banking app. You don’t need to understand blockchain technology to use Bitcoin, just like you don’t need to understand TCP/IP to use the internet.

“What’s the best time of day/week to buy?”

There isn’t one. Anyone who tells you “Bitcoin always dips on Sundays” or “Buy during Asian trading hours” is guessing. Dollar-cost averaging removes this question entirely.

“Should I use a crypto credit card to get rewards?”

Once you’re comfortable with crypto, yes. I use the Coinbase card and get 4% back in stellar or 1% in Bitcoin. But master the basics first.

“How do I handle the stress of watching prices?”

Stop watching. Check once a day maximum, preferably weekly. I removed all price tracking apps from my phone. My mental health improved dramatically, and ironically, my returns got better because I stopped making emotional decisions.

A Final Thought:

Ten years ago, I bought my first Bitcoin for the same reason you’re reading this article—I wanted to be part of something new, something potentially revolutionary.

I’ve made mistakes. Sold too early, bought too late, fallen for scams, panic-sold at bottoms, FOMO-bought at tops. I’ve experienced every emotion this market can throw at you.

But through it all, the people who’ve done well—including me—share one trait: We stayed patient, stayed educated, and stayed invested through the chaos.

Your Bitcoin journey starts with a single decision. Not how much to buy, but whether you’re ready to commit to learning and holding for the long term.

If you are, welcome to the ride. It’s going to be volatile, fascinating, occasionally terrifying, and potentially one of the best financial decisions of your life.

Just remember: Start small, stay secure, and think in years, not days.

Disclaimer: This article represents my personal experience and opinions after ten years in cryptocurrency. It is not financial advice. Cryptocurrency investments carry substantial risk of loss. Only invest what you can afford to lose completely. Always do your own research and consult with a licensed financial advisor before making investment decisions. Past performance does not guarantee future results.